💰 Don’t Sell Your Bitcoin – Borrow Against It: The Best Platforms in 2026

Get Breaking News First!

Editor’s choice

-

💰 Don’t Sell Your Bitcoin – Borrow Against It: The Best Platforms in 2026

-

MetaMask Who? The Web3 Wallets Traders Are Actually Using in 2026

-

💼 When Crypto Trading Becomes a Business: The IRS Rules Every Active Trader Needs to Know

-

₿ Why Local Businesses Are Taking Bitcoin Seriously in 2026

-

⚡ The Best of Both Worlds: How Hybrid Crypto Exchanges Are Changing the Way We Trade

-

The Taxman Cometh – Here’s How Smart US Traders Are Staying Ahead in 2026

Selling Bitcoin to access cash is a taxable event, a broken position, and a bet that you will be able to buy back at the same price or lower. Most of the time, that bet does not pay off.

Bitcoin-backed loans exist for exactly this situation. You keep your BTC, you access liquidity, and you repay on your terms. After a rough few years that took out several major platforms, the lending landscape in 2026 is leaner, more transparent, and considerably safer than it was.

Here is how to navigate it.

Join our community of 400K+ and never miss breaking news!

We respect and protect your privacy. By subscribing your info will be subject to our privacy policy . Unsubscribe easily at any time

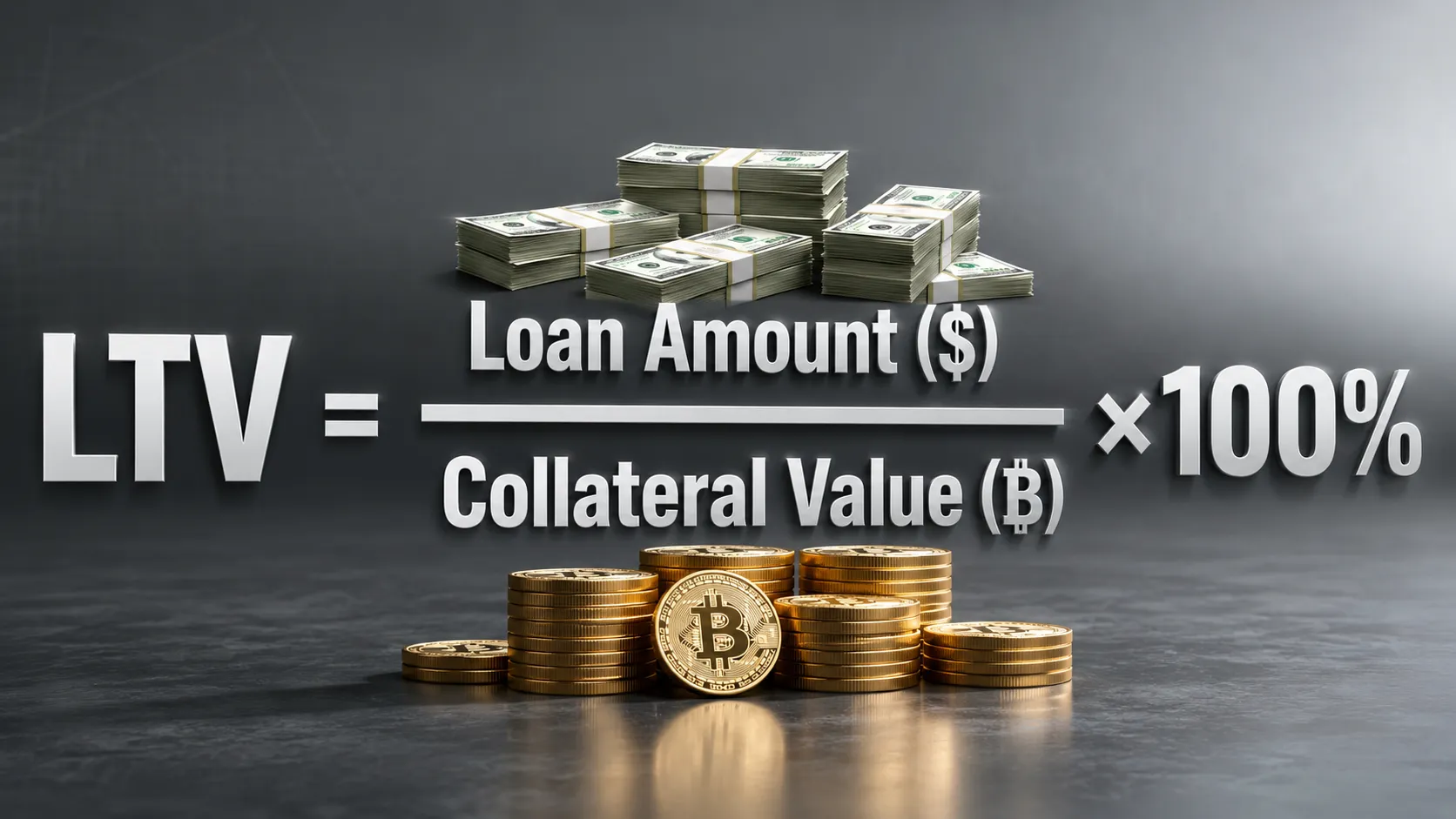

💵 How Bitcoin-Backed Loans Actually Work

The idea is simple.

You deposit Bitcoin as collateral and borrow against it, usually in stablecoins or fiat. Because the loan is overcollateralized, you need to lock up more value than you borrow.

For example, you might deposit $10,000 in BTC and borrow $3,000–$5,000, depending on the platform’s loan-to-value ratio. If the price of Bitcoin drops and your collateral ratio weakens, you’ll need to add more collateral, or risk liquidation.

That’s where most people get caught, because they focus on interest rates and ignore liquidation levels.

These setups are part of the broader world of crypto loans, where managing collateral matters more than the cost of borrowing.

🏦Top Bitcoin-Backed Loan Platforms in 2026

Ledn

Ledn is a simple, Bitcoin-focused lender that’s stayed consistent across cycles.

Focus: Bitcoin-only lending

LTV: Up to 50%

Best for: Long-term holders who want a transparent, conservative setup

Nexo

Nexo offers a more flexible, feature-rich environment with instant credit lines and variable rates.

It’s closer to a hybrid crypto bank, with the ability to repay anytime.

LTV: around 50% for BTC

Best for: Traders who want fast access to liquidity without rigid terms

Aave (DeFi Option)

For those staying fully on-chain, Aave is still a dominant player.

Offers algorithmic rates and full custody through smart contracts.

LTV: usually 65–75% max LTV depending on asset

Best for: Advanced users comfortable with DeFi

This is where how flash loans work becomes relevant at a high level. DeFi lending operates in the same composable ecosystem, even if you’re not directly using flash loans.

Join our community of 400K+ and never miss breaking news!

We respect and protect your privacy. By subscribing your info will be subject to our privacy policy . Unsubscribe easily at any time

Binance Loans

Still one of the most accessible options with high liquidity, competitive rates, and fast execution.

Best for active traders already operating within the Binance ecosystem.

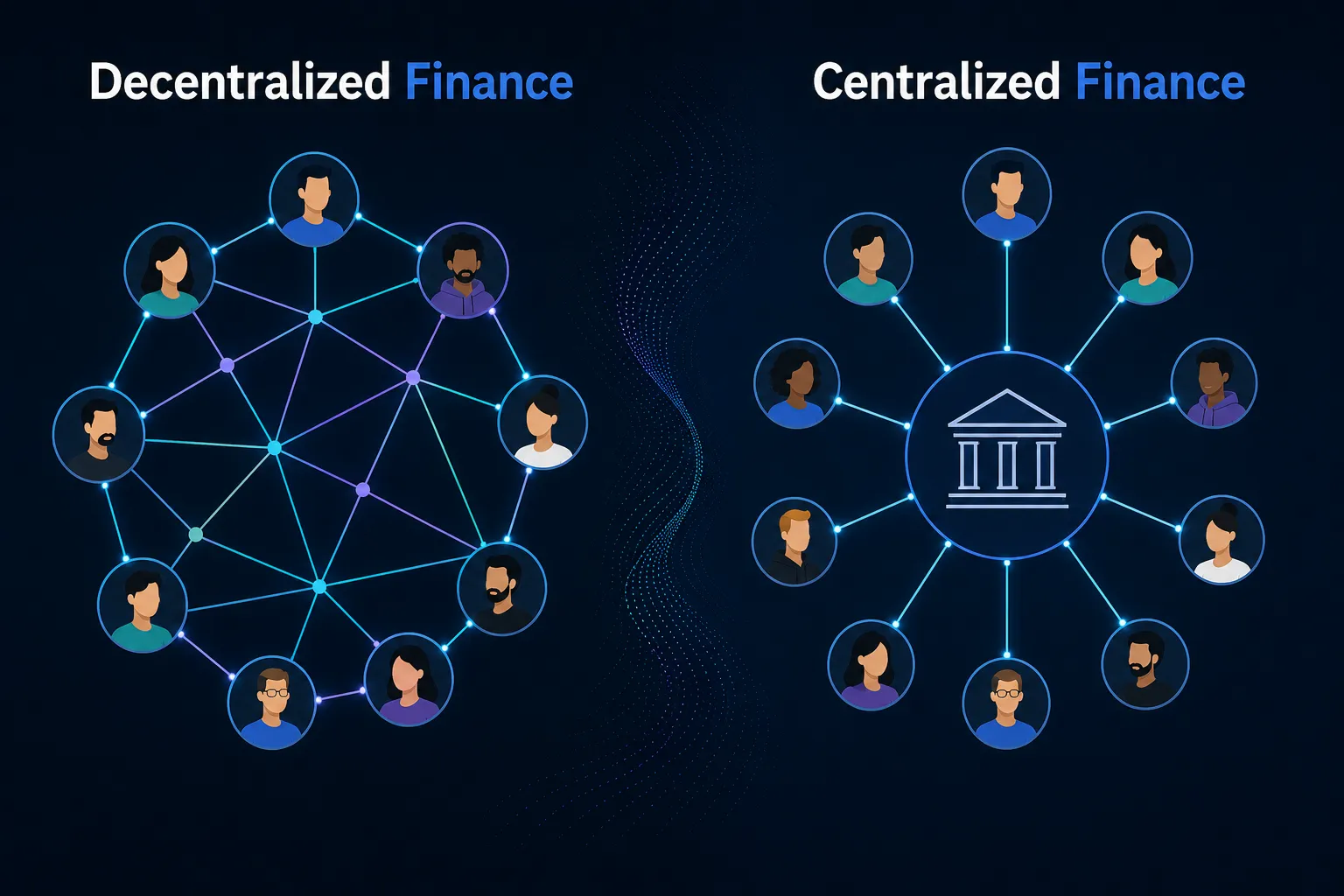

⚖️ CeFi vs DeFi: Where Should You Borrow?

This isn’t just preference, it’s risk tolerance.

CeFi (Ledn, Nexo, Binance):

DeFi (Aave):

Since 2024, many traders have moved back to CeFi for simplicity. But DeFi still appeals to those who don’t want to trust a centralized platform.

⚠️ Borrowing Against Bitcoin: Risk vs Reward

Borrowing against Bitcoin isn’t about interest rates. It’s about liquidation risk.

Bitcoin moves fast. A 20-30% drop can happen quickly, and if your loan sits too close to that level, you’re exposed.

That’s why LTV matters:

25% LTV = more buffer

50% LTV = higher risk

If you believe in Bitcoin long term, getting liquidated is the worst outcome. You lose your position when you wanted to hold it.

That’s also why people borrow instead of selling. Selling BTC for short-term cash can mean exiting a long-term position too early. Borrowing lets you keep exposure while still accessing liquidity.

You get:

You get to keep your position, but manage your risk.

🔐 Security and Platform Risk

Risk hasn’t disappeared.

Centralized lenders can fail. Smart contracts can break. Scams are getting more sophisticated, especially around phishing and fake platforms.

Basic rules:

✌🏼Conclusion

Bitcoin-backed loans are a genuine tool that offer liquidity without selling, with exposure intact. The variable most borrowers underestimate is not the interest rate. It is the liquidation candle they did not plan for.

Know your liquidation level before you borrow. Size accordingly and leave room for volatility.

For weekly capital strategy breakdowns, subscribe to the DayTrading.co newsletter. Already have that covered? 80k traders are waiting on our Telegram.