How to Invest in Crypto With an IRA? A Complete Guide

Get Breaking News First!

Editor’s choice

-

🔐 One Wallet for Everything Is How Most Traders Get Hurt. Here Is How Many You Actually Need

-

💰 Don’t Sell Your Bitcoin – Borrow Against It: The Best Platforms in 2026

-

MetaMask Who? The Web3 Wallets Traders Are Actually Using in 2026

-

💼 When Crypto Trading Becomes a Business: The IRS Rules Every Active Trader Needs to Know

-

₿ Why Local Businesses Are Taking Bitcoin Seriously in 2026

-

⚡ The Best of Both Worlds: How Hybrid Crypto Exchanges Are Changing the Way We Trade

Most traders obsess over entries, exits, and leverage — but ignore the biggest edge of all: taxes.

A Crypto IRA lets you hold Bitcoin inside a retirement account where gains grow tax-deferred or even tax-free. That sounds powerful. It is. But it comes with rules, custodians, and costs most traders overlook.

Here’s how Crypto IRAs actually work in 2026, and whether they’re worth it.

Join our community of 400K+ and never miss breaking news!

We respect and protect your privacy. By subscribing your info will be subject to our privacy policy . Unsubscribe easily at any time

💎 What Is a Crypto IRA?

A Crypto IRA is a self-directed IRA (SDIRA) that lets you buy Bitcoin and other cryptocurrencies inside a retirement account. You still get the same tax advantages — just with different assets.

It’s designed for long-term positioning, not rapid entries and exits. If your strategy revolves around short-term setups and active management, that’s closer to swing or day trading — which is a completely different framework than retirement investing.

🧨 How to Invest in Crypto With an IRA

✅ 1. Choose Your IRA Type

Before putting Bitcoin inside a retirement account, you need to choose the right IRA structure. This decision affects how and when you pay taxes.

🚨 2. Pick a Crypto IRA Provider

This is one of the most important decisions you’ll make in the IRA process: choosing the custodian that holds your crypto for decades.

Not all providers are equal. Some charge high annual fees that quietly eat into your returns. Others limit what assets you can buy or how you can trade.

Compare well-known options like iTrustCapital (lower fees, solid security), BitcoinIRA (easier onboarding but higher cost), and AltoIRA (a reasonable middle ground). Look closely at:

Security matters. $1.3 billion was stolen by North Korean hackers last year alone. So make sure your custodian isn’t the weak link.

📊 3. Fund Your Crypto IRA

You’ve chosen your custodian, now you need to fund the account.

There are three main options: roll over an old 401(k), transfer from another IRA, or contribute new cash (within annual limits).

Direct transfers are usually the safest route. The money moves straight from one provider to another, avoiding the 60-day rollover deadline and the 20% withholding that can apply to indirect rollovers.

If you’re moving funds from a 401(k), coordinate with your old plan administrator so the money goes directly to the new custodian. If a check is issued in your name, forward it immediately, because timing matters.

If you’re already holding crypto in another IRA, you may be able to request an in-kind transfer so assets move without being liquidated.

Join our community of 400K+ and never miss breaking news!

We respect and protect your privacy. By subscribing your info will be subject to our privacy policy . Unsubscribe easily at any time

One hard rule: you can’t withdraw funds, buy crypto personally, and then “put it back” into the IRA. All purchases must happen inside the account.

📌 4. Select Your Cryptos and Buy

Most Crypto IRA providers integrate with partner exchanges, allowing you to place trades inside the retirement account. You get to choose the assets, which typically includes Bitcoin, Ethereum, Solana, and a limited list of supported coins.

Execution is self-directed, but it happens within the platform’s system. You won’t be sending funds to external wallets or using outside exchanges.

Before placing trades, review the available assets, spreads, and trading fees. And if you need a refresher on how crypto buys actually work — including order types and execution basics — our guide on how to buy your first Bitcoin in the US walks through it step by step.

Retirement accounts are long-term vehicles — treat position sizing and asset selection accordingly.

💡Pros and Cons

Pros:

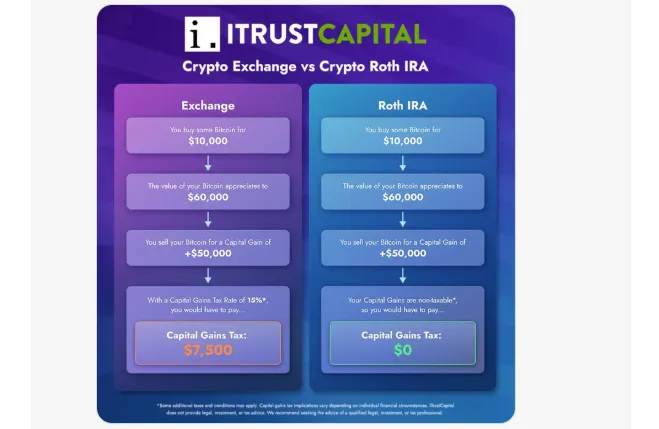

- You don’t get taxed every time you trade: Inside a Crypto IRA, buying and selling doesn’t trigger capital gains each move. In a normal brokerage account, every exit can create a tax bill.

- Compounding works harder: With a Traditional IRA, gains grow tax-deferred. With a Roth, qualified withdrawals can be tax-free. Over decades, that structure matters more than one good trade.

- Built-in long-term bias: Retirement accounts aren’t built for panic-selling. That structure can force discipline when markets get ugly.

Cons:

- You don’t control the keys: Your crypto sits with a custodian. No self-custody. No hardware wallet.

- You’re trusting a third party: If a provider fails or gets breached, your retirement funds are exposed. And unlike banks, Crypto IRAs don’t come with FDIC or SIPC protection.

- Volatility still hits: Tax advantages don’t cancel drawdowns. Bitcoin can drop 30–50% in a cycle, and your IRA balance will feel it.

🔖 Final Thoughts

A Crypto IRA isn’t about chasing hype. It’s about structure.

If you believe in Bitcoin long term, holding it inside a tax-advantaged account can meaningfully change your after-tax outcome. The edge isn’t just price appreciation, it’s how that growth is treated over decades.

Choose your provider carefully, understand the rules, and treat it like what it is: a long-term strategy, not a trading account.

Stay ahead of structural shifts in crypto and policy. 🚀 Join 60k traders on Telegram for immediate signals + fresh crypto intel in our weekly newsletter.